The real estate market in SW Montana remains resilient even amidst the headwinds of higher interest rates and continued low inventory. Buyers continue to actively pursue properties – with increased days on market and price negotiations have become more common. The market has balanced these forces and median sales price remains relatively stable. There are some areas where there was a ‘dip’ in 2023 that has now bounced back in line with where trends were in 2022. For the most part, 2022 still looks to have been the ‘peak’ of the market, however prices have adjusted little. The price negotiations happening now are keeping the sales prices rolling and stable instead of trending more steeply upward. List prices ‘escaping the barn’ are being walked back to these same stable trends.

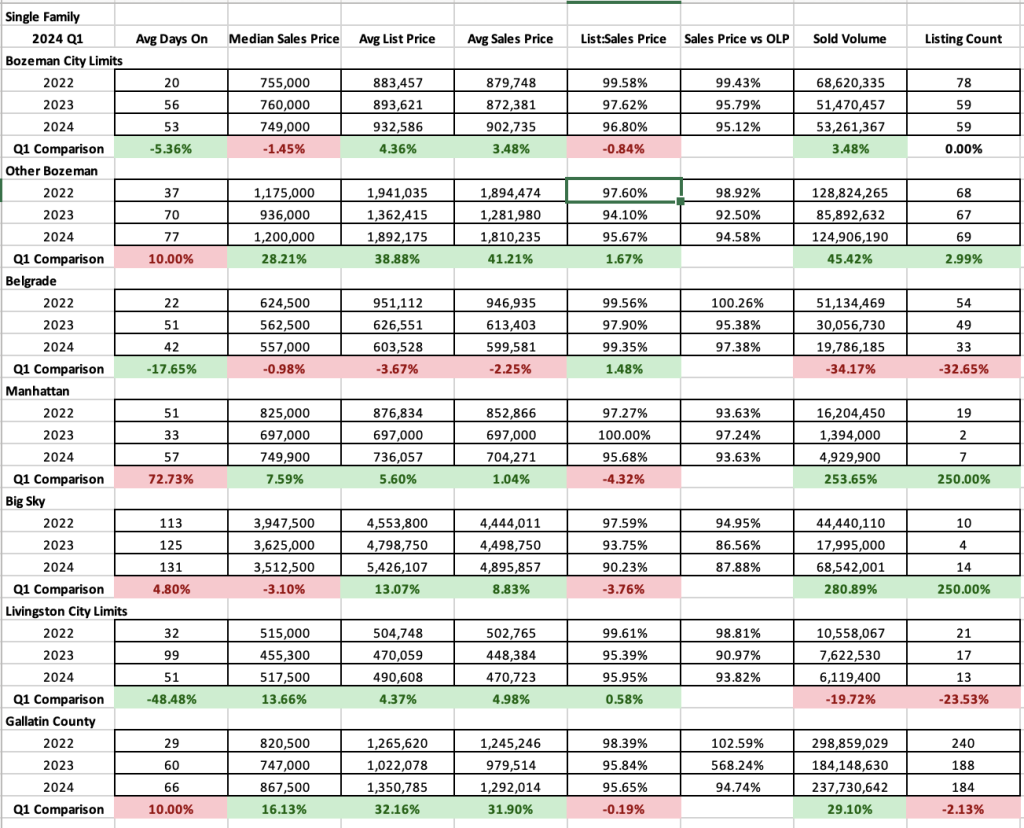

Single family

Single family home sale listing sold counts remain on par or slightly reduced, depending on area, comparing Q1 2023 and Q1 2024. There has been more marked activity in Big Sky. Overall, though on average it’s very comparable to 2023. Median sales prices were fairly flat comparing Q1 2022-2024 – some areas experiencing more of a dip in 2023 than others. Median sales prices for Q1 2024 were $749K in City of Bozeman, $1.2M in greater Bozeman outside of city limits, $557K in Belgrade, $750K in Manhattan, $3.5M in Big Sky and $517K in Livingston. List to sales price ratios – the percentage difference between what a property is listed for and what it sold for – show accelerated discounting between list and sales price in City of Bozeman (3.2% on average), Greater Bozeman (4.4% on average). Belgrade was the only area where the list to sales price ratios were less than 1% – showing a strong seller’s market in this area – possibly due to the affordability of the area. Interestingly there was a trend of increasing price adjustments in almost all areas prior to properties going pending – a sign of sellers continuing to push the price ceiling and prices snapping back to market trends. Number of units sold was essentially flat against either Q1 2023 or Q1 2022 or lower in all areas tracked.

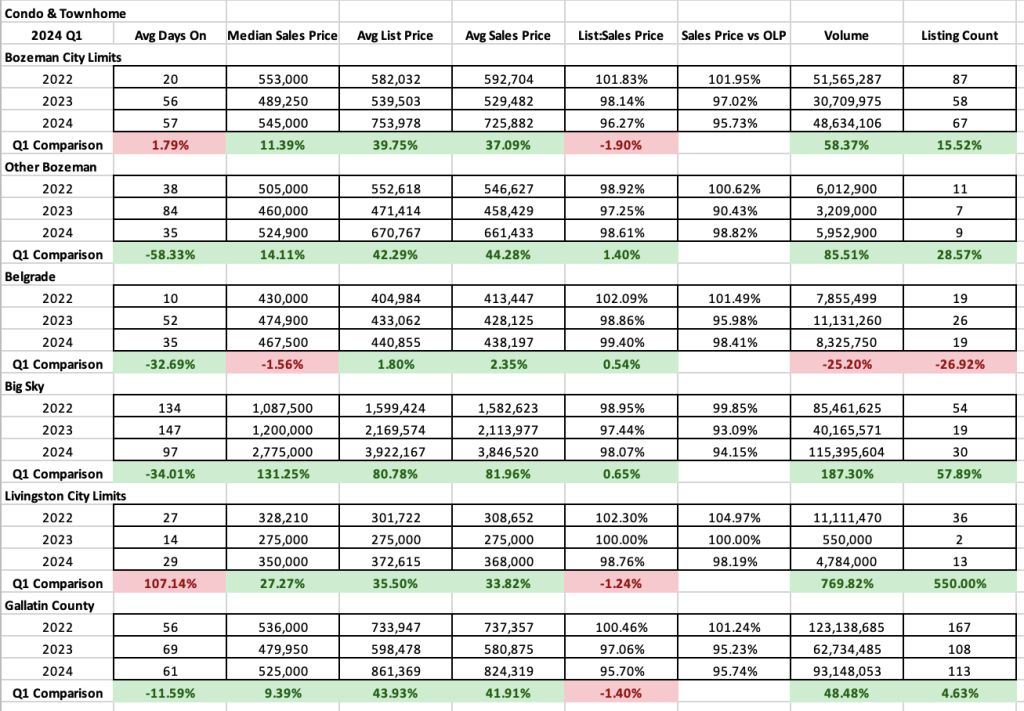

Condos/Townhomes

Condos and townhomes in Q1 2024 remained slightly muted over 2022 numbers for number of sales. 2023 saw a marked dip in most areas and 2024 has recovered some from the limited number of sales – showing a slight loosening of inventory. Median sales boosted after a dip in Q1 2023 in almost all areas, City of Bozeman at $545K, Greater Bozeman at $525K, Big Sky at $2.775M (a big jump, fueled by construction of luxury products in Moonlight), Livingston at $350K (spurred by continued condo construction in Livingston), and Belgrade at $467K (the only flat area). List to sales price ratios show increased discounting in some but not all areas – City of Bozeman (3.75% on average, adding another 0.5% if original list price is factored in) and Livingston (1.25% on average, adding another 0.5% if original list price is factored in) were the two areas with increased discounting off list price. The other areas tracked narrowed amount of discounting year over year. Big Sky at 2% off list price and 6% off original list price, Belgrade at 0.6% off list price and 1.6% off original list price and Greater Bozeman at 1.4% off list price. Number of listings sold increased in all areas over Q1 2023 (still lower in most cases than 2022).

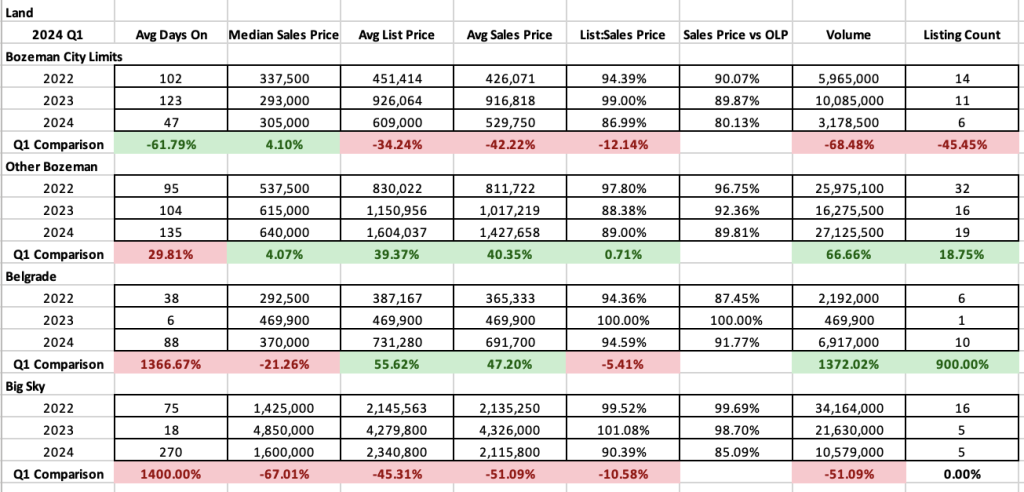

Land

Land has seen some more dramatic movement than residential product during Q1 2024. Median sales price jumped in Greater Bozeman ($640K) and City of Bozeman ($305K) and fallen in city of Belgrade ($370K – due to single family lots being available) and Big Sky ($1.6M). List to sales price ratios showed deep discounting off list price across all areas – at 13% in City of Bozeman (20% off original list price), 11% in Greater Bozeman, 5.5% in Belgrade (8% off original list price) and 10% in Big Sky (15% off original list price). Number of listings sold increased in greater Bozeman, remained flat in Belgrade and dropped off significantly in City of Bozeman.

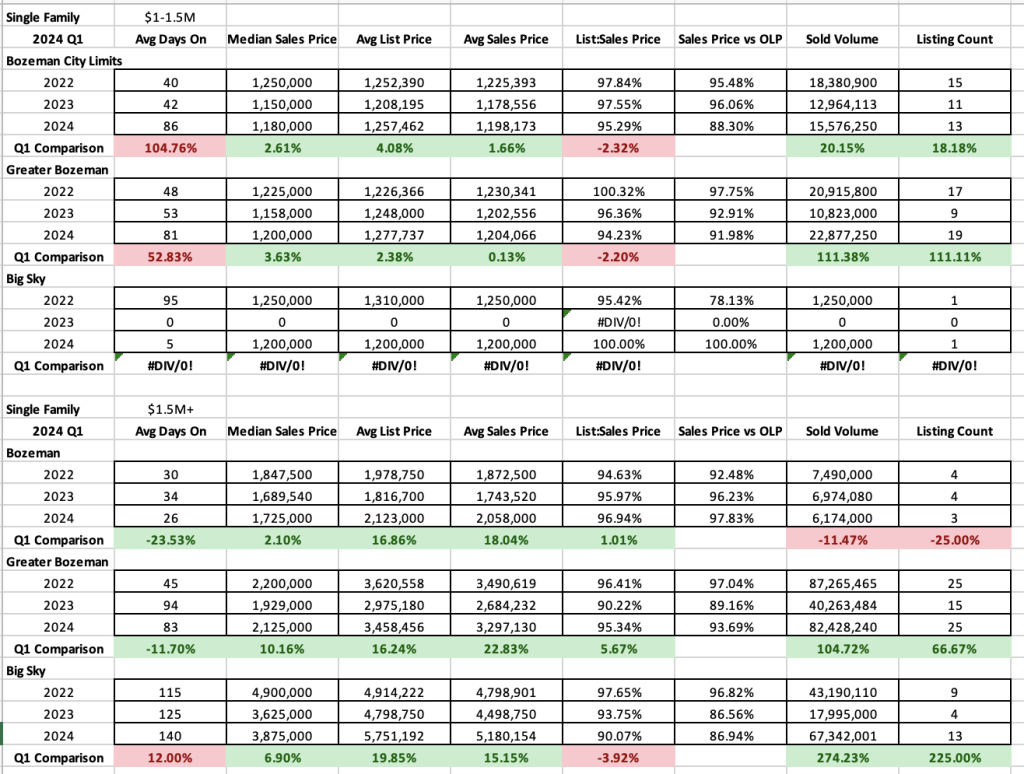

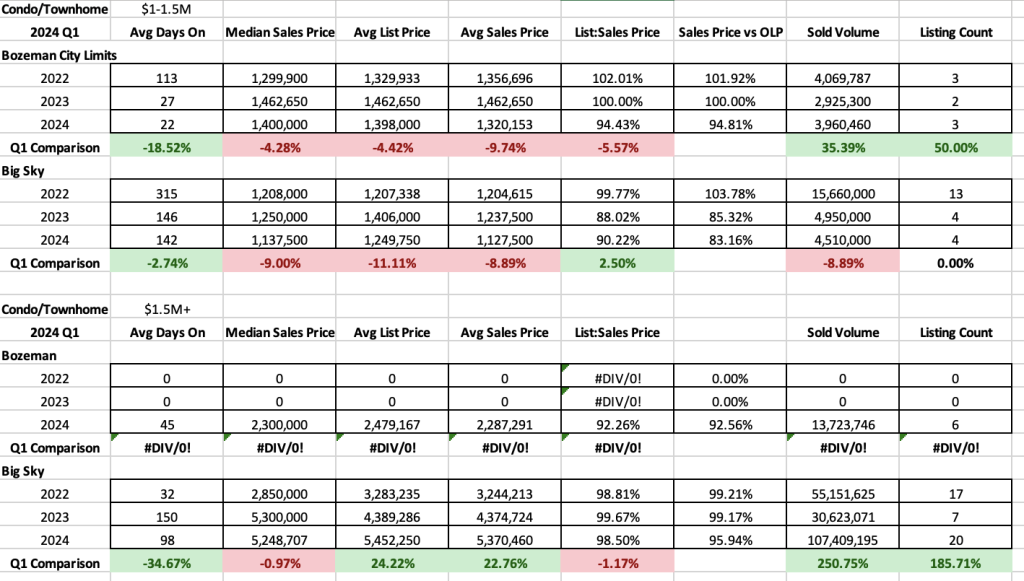

Luxury and High End

High-end single-family homes ($1M-$1.5M) saw an uptick in sales in City of Bozeman and Greater Bozeman Q1 2024 vs Q1 2023. List to sales price ratios showed more discounting off of list price than in Q1 2023 – on average 4.3% in City of Bozeman and 5.7% in greater Bozeman outside of city limits.

Luxury single family home sales ($1.5M+) stayed steady in City of Bozeman and had an uptick back to Q1 2022 number of properties sold in Greater Bozeman and surged beyond 2022 and 2023 in Big Sky for Q1. List to sales price ratios showed more discounting than in the past two years – with 3% on average in the City of Bozeman, 4.7% on average in Greater Bozeman and 10% in Big Sky.

High end condo and townhome sales ($1M-$1.5M) remained steady year over year in City of Bozeman and Big Sky – with more discounting on average off list price – City of Bozeman at 6.6% and Big Sky at 10%.

Luxury condo and townhome sales ($1.5M+) had a boost by new construction closings in the City of Bozeman and some resales. List to sales price ratios for Bozeman showed on average discounting of 7.7%. In Big Sky number of sales wase up significantly as several major new construction projects have come to completion – list to sales price ratios remained very competitive with only 1.5% discounting on average – many of these sales being new construction that wasn’t completed, there was little room for negotiation on price.